In a Periodic Review Inventory System How Many Units Are Ordered?

All the Formulas You lot Need to Get Started

The guide has everything y'all need to understand and use a periodic inventory system. You'll find bones journal entries, formulas, sample problems, guidance, expert communication and helpful visuals.

What Is Periodic Inventory?

Periodic inventory is an accounting stock valuation exercise that's performed at specified intervals. Businesses physically count their products at the end of the flow and use the information to rest their general ledger. Companies then apply the residuum to the commencement of the new period.

Under a periodic review inventory system, the bookkeeping practices are different than with a perpetual review system. To calculate the amount at the end of the year for periodic inventory, the company performs a physical count of stock. Organizations use estimates for mid-year markers, such as monthly and quarterly reports. Accountants do non update the full general ledger business relationship inventory when their company purchases appurtenances to exist resold. Instead, they debit the temporary account purchases. A temporary business relationship begins each twelvemonth with a naught remainder. The accountant removes the residue to another account at the end of the yr.

Companies brand any necessary adjustments from purchasing goods to a general ledger contra account. A contra account is meant to be opposite from the full general ledger because it offsets the balance in their related business relationship and appears in the financial statements. Examples of contra accounts include purchases discounts or purchases returns and allowances accounts. Combining these accounts provides the net purchases.

In a periodic inventory control arrangement, companies also continue delivery costs in a separate account from the master inventory account. They runway commitment costs related to incoming inventory Freight In or Transportation In accounts. Eventually, the costs in this business relationship increment the value of their inventory. In the journal, the accounts would look like this:

Key Takeaways

- Periodic inventory is an bookkeeping inventory method where inventory and cost of goods sold are calculated at the end of an accounting menses rather than on a daily basis.

- Periodic inventory systems can make sense for small to midsized businesses with a low number of products sold, while large and growing business opt for the perpetual inventory method and its college accuracy.

- Periodic tracking is like shooting fish in a barrel to implement just limits the details yous know about your inventory at whatever given time.

Periodic Inventory Explained

With a periodic inventory organisation, a company physically counts inventory at the end of each period to decide what's on hand and the price of goods sold. Many companies choose monthly, quarterly, or annual periods depending on their product and bookkeeping needs.

Rather than update their books with current inventory and cost levels on an ongoing basis, businesses have the first inventory level, catastrophe inventory and purchases made during that flow for cost calculations.

Periodic inventory works for businesses that don't need to accurately know current inventory levels on a daily basis. It works well for pocket-sized businesses looking to proceed costs low. Growing businesses and larger businesses demand more than detailed inventory tracking and typically choose a perpetual inventory arrangement, which is best managed using an ERP inventory module.

While it doesn't give business decision makers real-time information, periodic inventory is just fine for many small businesses, particularly those with few unique SKUs to update at the stop of each period.

What Is a Periodic Inventory System?

The periodic inventory organisation is a software organization that supports taking a periodic count of stock. Companies import stock numbers into the software, perform an initial physical review of goods and so import the data into the software to reconcile.

These software systems back up your current stock-keeping method. Y'all can apply them to get paper inventory lists, import the stock data and calculate the data you demand to order more stock and reconcile the stock you accept for a new period. Companies can export these figures and reports to accounting software. A company volition choose the software based on its needs and the requirements of its products.

Catherine Milner and Geoff Relph are co-authors of "Inventory Management: Advanced Methods for Managing Inventory inside Business Systems" and "The Inventory Toolkit: Concern Systems Solutions". Every bit owners of Inventory Matters, Ltd., they consult with clients and advise choosing a software system for inventory management that does the upfront work.

Milner explains: "We see many companies trying to implement inventory direction business systems that do non have the features or requirements they need. The most important thing is to know what you need precisely. When someone comes to sell you a organization, their measures of success may not be the same as your business concern's measure of success. Whether it is your business organization, the sales business or the hosting business organisation, each has a unlike focus. Then ensure yours is the ane that drives the auction."

Relph adds, "For example, when you buy a car, you know what you want. The salesperson may have a vehicle that does not exactly fit your request. His job is to persuade and sell you more y'all need. When you bulldoze away, you realize you cannot operate the vehicle finer. As a buyer, beware. You should buy what you need and not an approximation of what you think you want. Whether this happens as a matter of choice or misunderstanding, it inappreciably matters. This is not a criticism but is reflective of the industry."

Under a periodic organisation, the software should show the toll of inventory recorded as per the terminal physical count — it does not update based on sales. Companies register the purchases fabricated between counts in the purchases account. The software makes journal entries based on transactions out of the inventory and price of goods sold (COGS) accounts to user-defined accounts. Other features of periodic inventory software include:

- User-divers accounts gear up for dissimilar combinations of books and subsidiaries.

- Cosmos of journal entries in the background based on a scheduled script.

- Custom reports such as Journals Created Today, Journals Not Needed for Transactions Created Today, Error Reports and Modified Transactions.

- Customized software roles, such every bit the Principal Auditor.

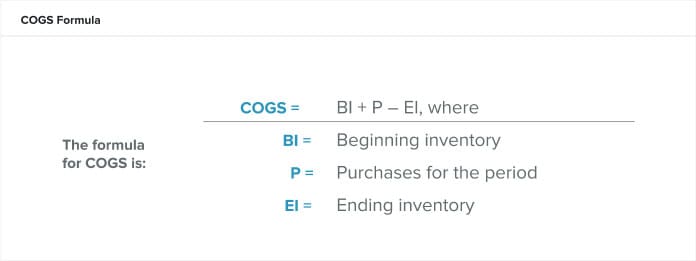

What Is the Cost of Sales?

The costs of sales are the straight expenses from the product of goods during a flow. These costs include labor and materials costs but exclude any distribution or sales costs. The formula for COGS, or costs of sales, is:

If you exercise non accept a true beginning inventory, calculate the beginning inventory every bit the remaining stock from the previous menstruum. The accounting menses can be in months, quarters or a agenda year. The COGS in a perpetual system is rolling, but you can calculate it for a flow.

Allow'south say our production manager, Cristina, wants to know if she is pricing her visitor'southward generic Bismuth subsalicylate loftier enough to leave a salubrious profit margin. If she calculates the COGS as $10 per 100-mL bottle, she will need to price each bottle higher than $x so her company can comfortably turn a profit.

Cristina's business uses the calendar year for recording inventory and records the beginning inventory on Jan. 1 and the ending inventory on December. 31. The company accountant valued the Jan. 1 beginning inventory of generic Bismuth subsalicylate at $49,000, or 4,900 bottles. During the twelvemonth, generic Bismuth subsalicylate costs the visitor $40,000 for materials and labor. On Dec. 31, the company accountants valued the catastrophe inventory at $thirty,000. Therefore,

When Is a Periodic Inventory System Used?

A minor visitor with a low number of SKUs would employ a periodic system when they aren't concerned nigh scaling their concern over time. Depending on your products and needs, you could also apply a periodic system in concert with a perpetual system.

Any business organization tin use a periodic system since in that location's no need for additional equipment or coding to operate it, and therefore it costs less to implement and maintain. Farther, yous can train staff to provide simple inventory counts when time is limited or you have high staff turnover. For example, seasonal staff may come and go. They can quickly count the goods they are working with, whereas a perpetual system, which provides a more accurate inventory, requires training staff on electronic scanners and information entry. Acquire more about a perpetual system and how it gives a more precise inventory solution past reading our "Guide to Perpetual Inventory".

Yous tin also use a periodic system if you have a handle on your supply chain process, sell a few products and accept eyes on your goods equally they flow through your business. A periodic system isn't useful if y'all demand to investigate to identify missing inventory or unbalanced numbers. This outcome will ascend as your operation grows and becomes more challenging to command positively.

Milner describes periodic systems as "a simple arroyo to inventory management which is useful for those small organizations which take a simple arroyo to inventory management. These businesses don't necessarily have a defined relationship between the raw materials or purchased items and the final sold product. One example of a business that would use a periodic system is a food bank. They would ofttimes count the concrete inventory to determine the endmost inventory quantity."

The Benefits of a Periodic Inventory System

The main benefits of employing a periodic inventory arrangement are the ease of implementation, its lower cost and the subtract in staffing needed to run it. Information technology only takes a picayune time to add a periodic system to your business. Simple counts on legal paper can suffice for collecting product data, especially if you only offer a few appurtenances. A bones count during the twenty-four hours or week is often plenty for a modest business to go an adequate handle on their inventory. This means there is no need for expensive or complicated equipment, simply essential information collection tools – pen and paper.

One big negative, however, is that you are merely collecting minimal information, unremarkably only a discrete product count. Further, you do not collect or report this data in "existent-time." You update stock numbers at singled-out periods and not when you buy or sell them. In fact, yous will not have much information to continue should you need to rails your products from commencement to cease or investigate shortfalls or overages. You can't quickly identify the source of problems.

Other negatives with a periodic system include:

- Errors in Estimation: In the periods between stock inventories, you must gauge the cost of appurtenances sold and which products and quantities are available. This estimate may be far from the actual COGS once you lot have completed a physical count.

- Pregnant Adjustments: In the periods between stock-taking, at that place is no fashion to account for losses, overages or obsolete appurtenances. This could upshot in substantial, plush adjustments after your next physical count. The only fourth dimension a periodic system is current is directly later on the stock-taking and the accounting events.

- Inability to Scale: A periodic organisation does permit for some room to grow, equally it is based on your power to rail your goods. However, scaling your business organisation with a periodic system becomes more fourth dimension-consuming and onerous every bit y'all grow and add together products to your inventory.

Challenges of Periodic Inventory

While periodic inventory is piece of cake to implement, it comes with several noteworthy drawbacks around the level of detail you lot go and how frequently your information is updated.

To make good business organisation decisions, near business concern owners and managers need updated information on a very regular basis. Most large businesses update inventory automatically with each sale or shipment. This is easily achieved with a modern ERP. Whenever you make a purchase at a retail shop or online, the retailer knows exactly what was sold and when and then it tin can make decisions around restocking.

Businesses with periodic inventory in place may not realize a production is running low until a client asks why it isn't on the shelf. Even worse, yous could make an online auction simply to find the item isn't in stock and backordered with your supplier. Both are far from ideal customer experiences and tin can add extra stress on your staff.

Even many small businesses utilise inventory tracking systems tied to their point of sales (POS) or online store. When the cashier scans a barcode and a client walks out with a product, the inventory is automatically updated. Sophisticated businesses may setup automatic reordering so they never run out of stock.

The ongoing data also helps businesses keep more than granular information on cost per item sold, which is a major factor in turn a profit margins and overall profitability. For large businesses or growing businesses, operating with a periodic inventory system is akin to operating your business organisation with blinders. Y'all don't accept the full film until the end of the menstruation.

What Is a Perpetual Inventory Organisation?

A perpetual inventory arrangement is a software system that continuously collects data about a company's products. A perpetual organization tracks every transaction as information technology happens, including purchases and sales. The arrangement also tracks all data pertinent to the product, such as its physical dimensions and its storage location.

A perpetual system is more than sophisticated and detailed than a periodic system because information technology maintains a constant record of the inventory and updates this record instantaneously from the point of sale (POS). Nevertheless, perpetual systems require your staff to perform regular recordkeeping. For example, in a periodic system, when you receive a new pallet of goods, yous may not count them and enter them into stock until the adjacent physical count. In a perpetual system, y'all immediately enter the new pallet in the software and then the system can track its life in your business organisation. When at that place is a loss, theft or breakage, you should besides immediately record these updates.

According to Relph, "When an organization grows such that all items require a SKU (e.m. internet sales), and then information technology is highly likely this business organization will need to move towards a perpetual inventory organisation."

A perpetual system is superior to a periodic system in many means, particularly for companies that are considering their longevity. Implementing a perpetual organisation earlier in the company's inception enables staff to have a long-term tape of the inventory and likewise keeps the business from growing out of a periodic system one day. A perpetual system can calibration, so whether you lot have five products (today) or 200 products (tomorrow), a perpetual organization can finer manage inventory control.

Periodic vs. Perpetual Inventory Systems

Periodic and perpetual inventory systems are dissimilar accounting methods for tracking inventory, although they can work in concert. Overall, the perpetual inventory arrangement is superior because it tracks all information and transactions. Yet, with a perpetual arrangement, you demand to make more decisions to use information technology successfully.

"Periodic systems are better with unknowns. Non all periodic systems have computer systems attached since computer logic does non exercise well with many unknowns," explains Relph. "One time your concern grows, yous need to define those unknowns to make a perpetual system work. You must define the products, assign SKUs and and so make decisions nigh the relationships between what you buy and sell."

Between the ii accounting systems, in that location are differences in how you update the accounts and which accounts you need. In a perpetual system, the software is continuously updating the general ledger when at that place are changes to the inventory. In the periodic arrangement, the software but updates the general ledger when you enter information after taking a concrete count. In a perpetual system, the COGS account is electric current after each sale, even between the traditional accounting periods. This method also makes the calculations less time-consuming. In the periodic organisation, you lot but perform the COGS during the accounting period.

One other primal difference between the two systems is the accounts yous use. In a perpetual system, you record purchases or inventory under the merchandise or raw materials account when you make them, updating the unit count entry for the private record, whereas in a periodic system, you lot document purchases into a buy asset account, which means an individual tape for unit of measurement counts isn't available.

Examples of Periodic Transaction Journal Entries

In a periodic inventory organisation, you lot update the inventory remainder once a menses. Typical journal entries for this organisation are simple. You can assume that both the sales and the purchases are on credit and that yous are using the gross profit to record discounts.

The gross profit method is an judge of the catastrophe inventory in the menses. You can use this in the acting period, the time between physical counts, or to estimate how much stock you lost in the example of a catastrophic event. This adding is an judge. Accountants do not consider it as an closed method to determine the annual inventory balance, as it is not precise plenty for fiscal argument reporting.

Follow these steps to calculate the gross profit judge:

- Calculate the cost of goods available for sale (COGAFS): Add the beginning inventory (BI) and the price of purchases (P) for the catamenia (COGAFS = BI + P).

- Estimate the cost of goods sold (COGS): Multiply the sales (South) for the flow by [1 – the expected gross profit % (EGP%)]. This calculation gives you COGS = Southward * (1-EGP%).

- Judge the ending inventory: Subtract the COGS from the COGAFS, or step #i – step #2 (EI = COGAFS – COGS).

In a periodic organisation, you enter transactions into the accounting journal. This periodical shows your company's debits and credits in a simple column course, organized by date.

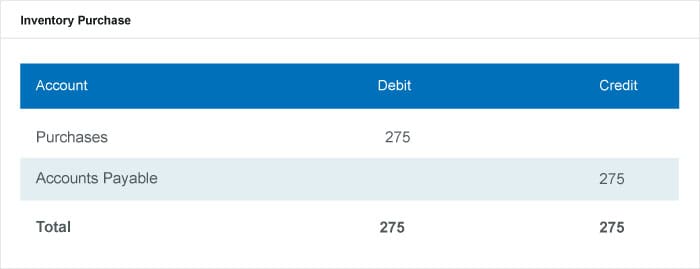

Record the purchase of inventory in a journal entry by debiting the purchase business relationship and crediting accounts payable.

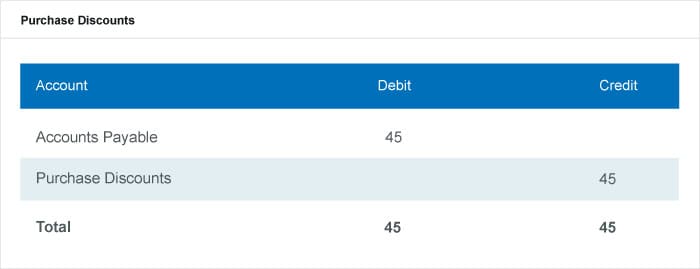

Tape the buy discount by debiting the accounts payable business relationship and crediting the purchase discount account.

Record the total accounts payable purchase and accompanying discount in an entry together that debits the accounts payable and credits the buy discounts account.

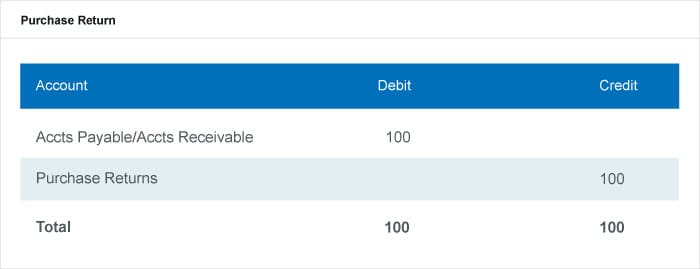

Tape the purchase returns by debiting the accounts payable or accounts receivable account and crediting the purchase returns account.

Record inventory sales past crediting the accounts receivable account and crediting the sales business relationship.

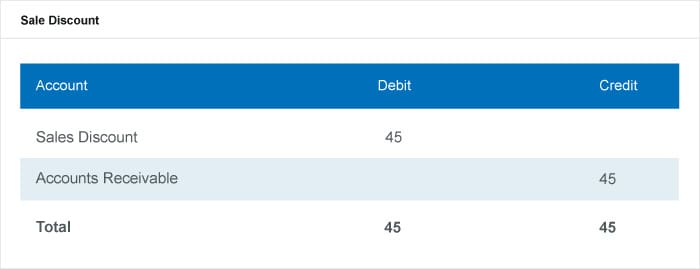

Record sales discount by debiting the sales discount account and crediting the accounts receivable business relationship.

Record your total disbelieve in your periodical past combining the inventory sales and the sales discount entries.

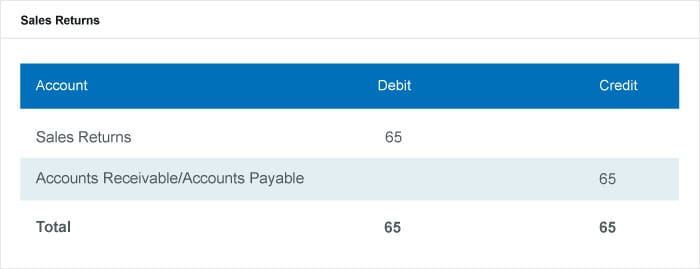

Record your sales return by debiting your sales returns business relationship and crediting your accounts receivable or accounts payable.

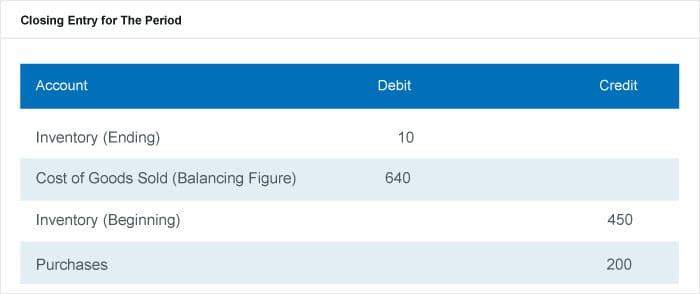

Consummate the closing entry at the finish of the accounting period, after the physical count. Y'all can calculate the COGS by using a balancing figure or the COGS formula. In this entry, the debits are in the ending inventory rows and the COGS row, and the credits are in the beginning inventory and the purchases rows.

Example of Periodic Systems

Periodic organization examples include accounting for beginning inventory and all purchases made during the flow as credits. Companies do not record their unique sales during the period to debit just rather perform a concrete count at the end and from this reconcile their accounts.

Cost flow assumptions are inventory costing methods in a periodic system that businesses use to calculate COGS and ending inventory. Outset inventory and purchases are the input that accountants utilize to calculate the cost of goods available for sale. They then employ this figure to whichever cost flow assumption the business chooses to use, whether FIFO, LIFO or the weighted average.

Cost Flow Assumption Diagram

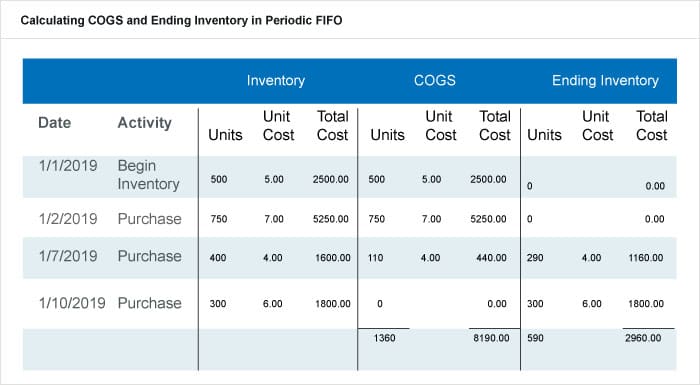

Periodic FIFO

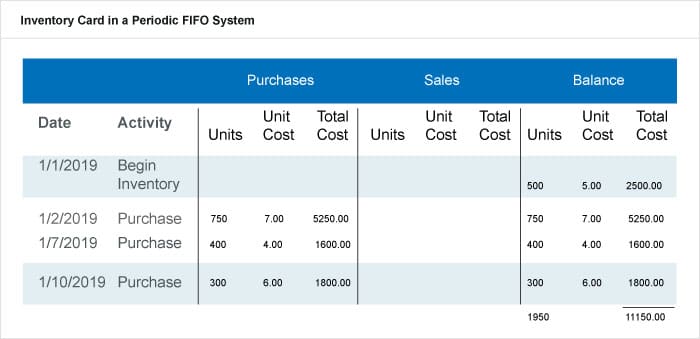

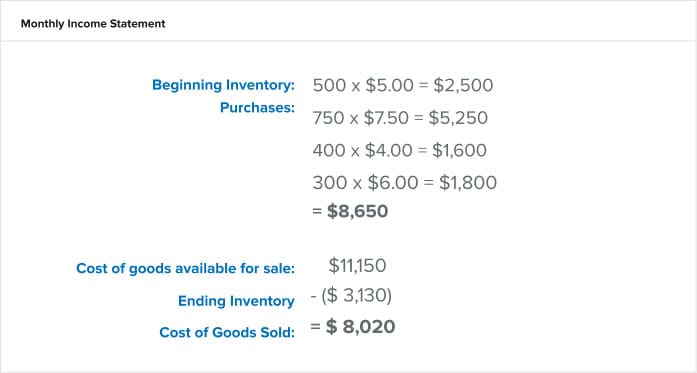

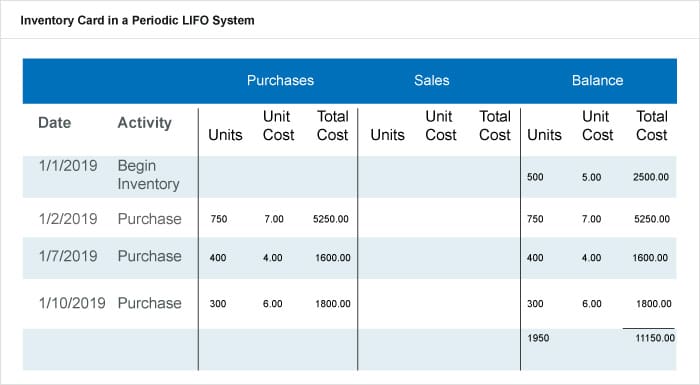

FIFO means get-go-in, first-out and refers to the value that businesses assign to stock when the first items they put into inventory are the first ones sold. Products in the ending inventory are the ones the visitor purchased most recently and at the almost recent price. In a periodic FIFO inventory system, companies apply FIFO by starting with a physical inventory. In this case, let's say the physical inventory counted 590 units of their product at the finish of the period, or January. 31. Purchases over this period are in the following table.

Over January, this visitor had 1,950 units from the start inventory and purchases. A periodic system doesn't track each auction during this menstruum. Therefore, 1,950 units – 590 units from the physical count = 1,360 units. This number is how many units you expect have been sold and should expect to be in COGS.

This company pulled into COGS the full purchases and costs from one/1/2019 and i/2/2019 and merely pulled what they required from the 1/seven/2019 buy to meet their calculated COGS amount from above (110 units). In a FIFO organisation, this company uses the first inventory in earlier they move to more contempo inventory (and prices). It put leftover units into the ending inventory, making information technology 590 units at $2,960 that it will also put into the offset inventory for the adjacent period.

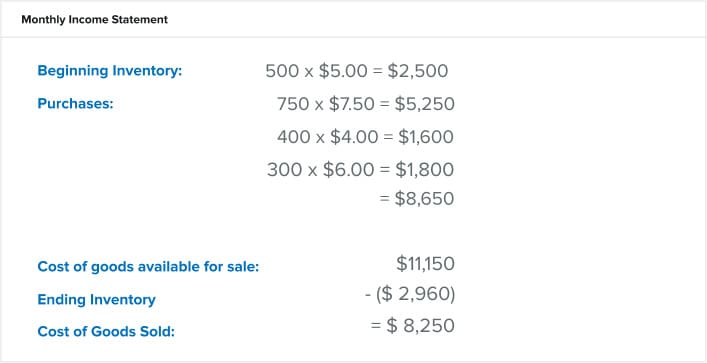

This company volition list the following figures on its monthly income statement:

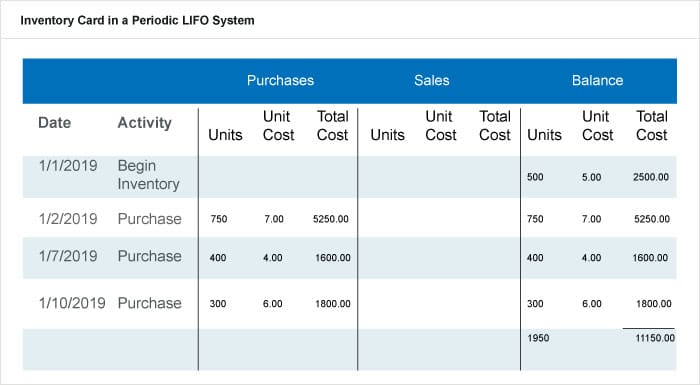

Periodic LIFO

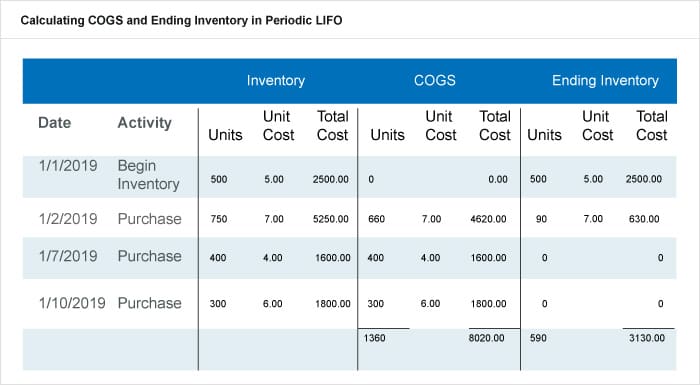

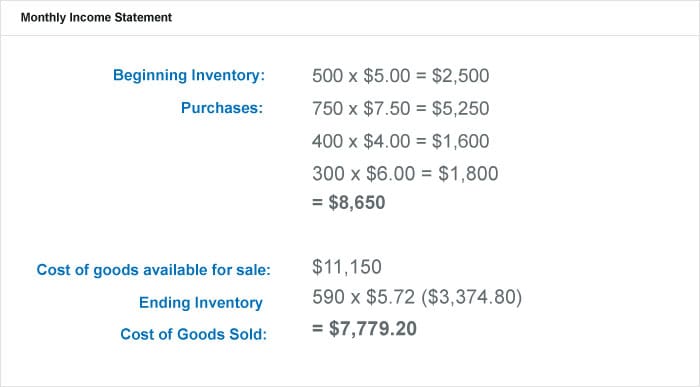

LIFO means final-in, first-out, and refers to the value that businesses assign to stock when the last items they put into inventory are the first ones sold. The products in the ending inventory are either leftover from the offset inventory or those the visitor purchased earlier in the period. LIFO in periodic systems starts its calculations with a concrete inventory. In this example, nosotros as well say that the physical inventory counted 590 units of their product at the end of the menstruum, or January. 31. Nosotros use the same table (inventory card) for this instance equally in the periodic FIFO instance.

Over January, this visitor had one,950 units from the start inventory and purchases. Yous don't worry almost tracking each sale during this catamenia. Therefore, 1,950 units – 590 units from the physical count = 1,360 units. This amount is the number of units that you expect are sold and should wait to be in COGS.

Different from a FIFO system, a LIFO system pulls the latest purchases into the COGS calculation. The auditor took the purchases last fabricated 1/x/2019, 1/seven/2019, and 660 units from 1/2/2019 and put them into COGS with their accompanying costs. Leftover items going into the catastrophe inventory were ninety units from the ane/2/2019 purchase and what was in the beginning inventory, giving the 590 units. This visitor counted the total cost of $three,130, which will get into the beginning inventory for the next period. Hither'south how they will list the following figures on their monthly income statement:

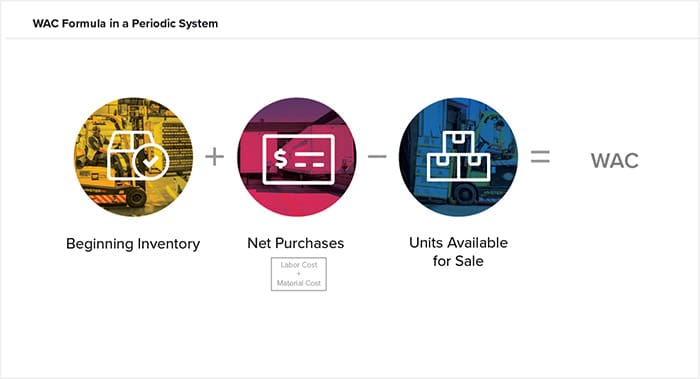

Periodic Weighted Average Costing (WAC)

Weighted average cost (WAC) in a periodic system is another cost flow assumption and uses an average to assign the ending inventory value. Using WAC assumes y'all value the inventory in stock somewhere between the oldest and newest products purchased or manufactured.

The formula is WAC = BI + P / units for sale

To maintain consistency, we'll use the aforementioned instance from FIFO and LIFO above to the calculate weighted average. In this example, the concrete inventory counted 590 units of their production at the end of the period, or January. 31. The same tabular array for this is below.

Before going further, the company calculates the weighted average of the purchases over the catamenia from the total cost divided by the total units over the period, or $11,150/one,950 units = $5.72 per unit of measurement. From this figure, it would contain the physical inventory the company counted of 590 units. Here is how it volition listing the following figures on its monthly income statement:

As yous tin can run into, weighted average in a periodic system is a calculation done outside of the ledger. In this method, you summate an average for the period instead of moving transactions over when the visitor bought or sold something during the period.

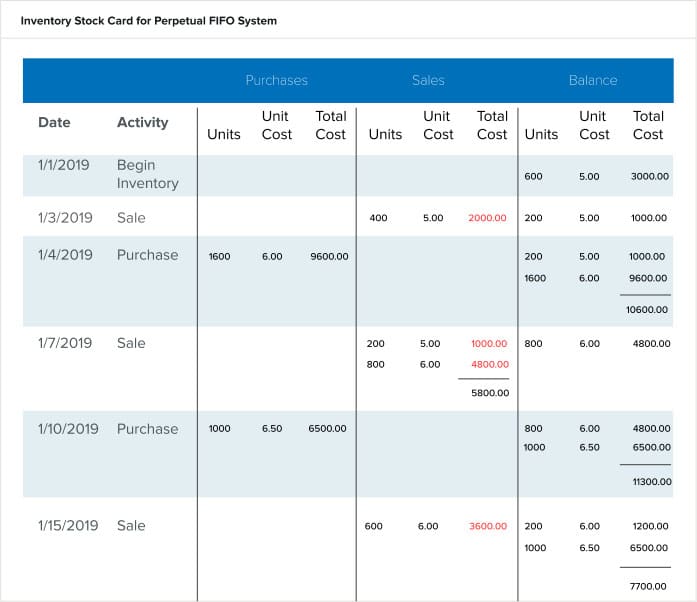

Perpetual FIFO

In a perpetual FIFO system, the company includes the sales as they happen in the ledger. The company should still perform physical inventories, just only to confirm the accuracy of the ledger'south data. They would perform these either yearly or past cycle counting. The biggest difference in the ledger in a perpetual system as compared to a periodic organisation is that the balance is a running tally of not but the units but the value (or full cost) of those units. The unit price moved over in the balance is based on when the stock sold comes in. Stock maintains the value the visitor purchased it for throughout its lifecycle in the company. For case, stock purchased on 1/4/2019 for $vi.00 per unit of measurement maintains that value through its sale. Come across the running tally in the chart below.

At the end of the period, the ending inventory is already calculated every bit the concluding entry. For this period, it is i,000 units at a total cost of $7,700.00. The toll per unit is $half-dozen.fifty, or the last purchase unit cost for the period. You'd calculate COGS from this ledger by going to the Total Cost in the Sales column and calculation the figures for what the company sold during that flow. These are the figures in red, or $2,000 + $1,000 + $4,800 + $iii,600 = $11,400.

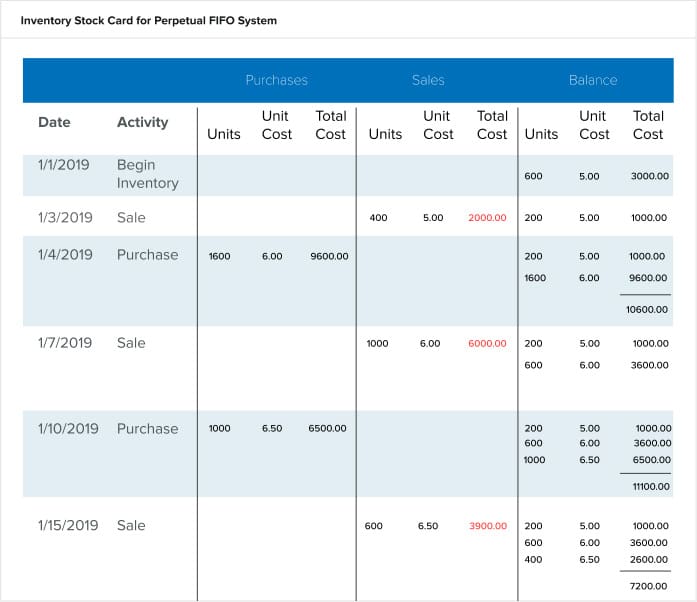

Perpetual LIFO

In a perpetual LIFO system, the company also uses the running ledger tally for purchases and sales, but they sell the inventory that they last purchased before moving to older inventory. In other words, the cost of what they sell is the same as what they about recently paid for that inventory. Meet the same activities from the FIFO card in a higher place in the LIFO card beneath.

Notice the deviation in the unit toll of the sales and what carries over to the remainder. The sales transaction on 1/7/2019 is most notable. The FIFO bill of fare noted two carve up transactions of sales (for 200 units at $5.00/unit and 800 units at $6.00/unit) under two different costs. In the LIFO carte, there was enough inventory at the nigh recent cost ($6.00 per unit) to fulfill the sales request past the single entry. This entry is for the nigh recently purchased inventory at the most recent price.

Tally the ending inventory shown at the bottom of the bill of fare. It is 1,200 at three different unit of measurement costs, adding up to $seven,200 for the period. Calculate the COGS by adding the Total Costs in the Sales column (the figures in red). COGS reflect what the visitor sold by the actual prices the units sold for. Therefore, COGS = $2,000 + $6,000 + $iii,900 = $eleven,900.

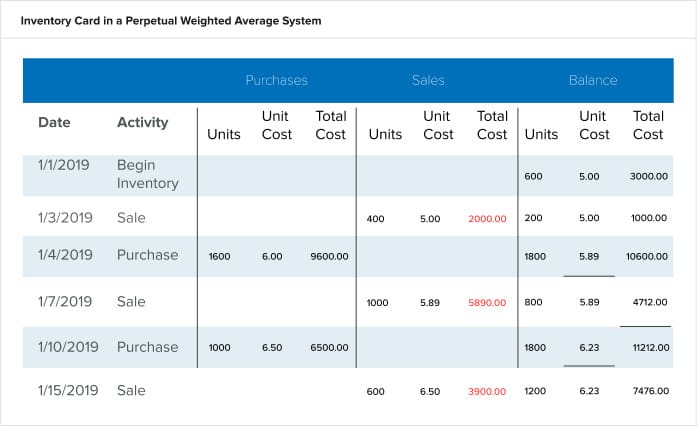

Perpetual Weighted Average Costing

In a perpetual weighted average calculation, the company keeps a running tally of the purchases, sales and unit costs. The software recalculates the unit price afterward every purchase, showing the current balance of units in stock and the average of their prices. The next sales transaction reflects this newly calculated unit cost. Run into the same activities from the FIFO and LIFO cards higher up in the weighted average carte du jour below.

Notice the deviation in the unit toll subsequently every purchase. The system recalculates the unit price and value of total cost based on the average of what is still in stock and what the company has added in their purchase. The ending inventory figure is the last numbers on the card: 1200 units at $7,476.00. Calculate COGS past adding the total costs of what the company sold (in red). COGS = $two,000 + $5,890 + $three,900 = $eleven,790.

Specific Identification

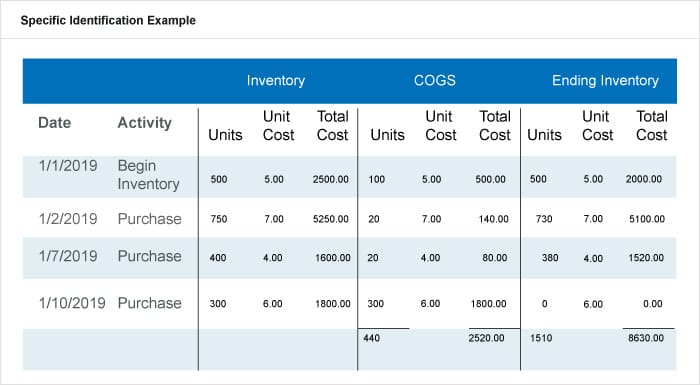

The specific identification method is the same in both a periodic system and perpetual system. Although not widely used, this method requires an extremely detailed physical inventory. The company must know the total units of each good and what they paid for each item left at the end of the period. In other words, the visitor attaches the actual cost to each unit of its products. This is unproblematic when the products are large items, such as cars or luxury applied science goods, considering the company must give each unit a unique identification number or tag.

The example below has the same activities as to a higher place, except the company tracks each unit individually and what it purchased. Then, information technology performs a detailed physical inventory, reporting back each unit sold past the date the purchase was made.

They study the ending inventory for each purchase appointment offset, and so add them up. The ending inventory for this flow is $2,520 for 440 units. Calculate COGs for each line detail, and then add them together to become the menstruum'southward COGS. In this instance, COGS is $8,630.00.

NetSuite Can Assist Provide Visibility Into Your Inventory

Properly managing inventory tin can make or pause a business, and having insight into your stock is crucial to success. While the periodic method is acceptable for companies that accept minimal inventory items or pocket-size businesses, those companies that plan to calibration will need to implement a perpetual inventory organisation. Regardless of the blazon of inventory command procedure you choose, determination makers need the right tools in place so they can manage their inventory effectively. NetSuite offers a suite of native tools for tracking inventory in multiple locations, determining reorder points and managing safety stock and cycle counts. Find the right residuum between need and supply across your unabridged system with the demand planning and distribution requirements planning features.

Acquire more nigh how y'all can manage inventory automatically, reduce handling costs and increase cash flow.

Periodic Inventory FAQs

What is periodic inventory organisation with an instance?

A periodic inventory system is an accounting method where inventory tracking is updated manually at the end of a specific period. For case, a small retail store with one location may choose periodic inventory to brand tape keeping simpler and may choose to update their inventory records on a quarterly basis for estimated tax calculations.

What is periodic inventory taking?

Periodic inventory taking is the physical count of inventory that takes place on a periodic schedule when using a periodic inventory method. Even businesses using perpetual inventory may desire to take a physical inventory count periodically to account for shrinkage (theft, broken, and lost items).

What is the difference between periodic and perpetual inventory?

Businesses using periodic inventory update their inventory records on a regular schedule, frequently monthly, quarterly, or annually. Perpetual inventory requires regular updates but offers more in-depth and timelier inventory information.

Who would apply a periodic inventory organization?

Periodic inventory systems are best for smaller businesses with just a few products to track. As businesses grow and track more unique SKUs, periodic inventory systems go less viable.

Source: https://www.netsuite.com/portal/resource/articles/inventory-management/periodic-inventory-system.shtml

0 Response to "In a Periodic Review Inventory System How Many Units Are Ordered?"

Post a Comment